Outcome Bias in Trading: Why a Winning Trade Is Not the Same as a Good Trade

A trader closes a position for a nice profit after doubling down on a losing trade. The account is green. The feeling is good. So the conclusion is obvious: that was a smart move. Time to do it again next time.

That conclusion is wrong. And it is one of the most dangerous conclusions a trader can reach.

This is the outcome bias at work. It is one of the most well-documented cognitive biases in decision science, first demonstrated by Baron and Hershey in 1988 across a series of five experiments. Their finding was straightforward: people consistently rate a decision as higher quality when they know the outcome was favourable, even when they have full access to the decision-maker's reasoning and information. The same decision, the same logic, the same probabilities. The only thing that changed was whether it happened to work out. And that was enough to shift how people judged it.

In trading, this bias does not just distort how you evaluate a single trade. It distorts how you evaluate your entire strategy. It is the reason traders abandon systems that are working and adopt systems that are not. And unlike most trading mistakes, it feels like learning.

What is outcome bias?

Outcome bias is the tendency to judge the quality of a decision based on its result rather than the quality of the reasoning behind it. A decision that was reckless but got lucky is rated as smart. A decision that was sound but ran into bad luck is rated as foolish.

The bias shows up everywhere, not just in trading. In medicine, a surgeon who performs a risky but well-reasoned operation is judged more harshly if the patient dies than a surgeon who performs the same operation and the patient survives. The reasoning was identical. The probabilities were identical. Only the outcome differed. But people cannot help themselves. They use the result to rewrite their evaluation of the thinking.

It is worth distinguishing outcome bias from hindsight bias, because they are often confused. Hindsight bias distorts your memory: it makes you believe you saw the result coming all along. Outcome bias is different. It distorts your evaluation of the decision itself. You might fully acknowledge that you had no way of knowing what would happen, and still judge the decision as better or worse depending on the result.

The research on this is consistent across fields. A study published in Management Science found that NBA basketball coaches are 17% more likely to change their starting lineup after a narrow loss than after a narrow win, even though the difference between losing by one point and winning by one point is essentially random. A separate study in football found that players were rated substantially better across an entire match if they happened to score a lucky goal versus hitting the post and missing. Same player, same performance, same 90 minutes. One bounce of a ball changed how the whole match was evaluated.

Annie Duke, a former professional poker player and decision strategist, made this point clearly in her book Thinking in Bets. If a skilled poker player and a weak poker player play for eight hours, the weaker player still wins over 40% of the time. An observer watching only the outcome of that session would conclude the weaker player is the better one. This is outcome bias in its purest form: confusing who won with who played better.

How do good and bad decisions relate to good and bad outcomes?

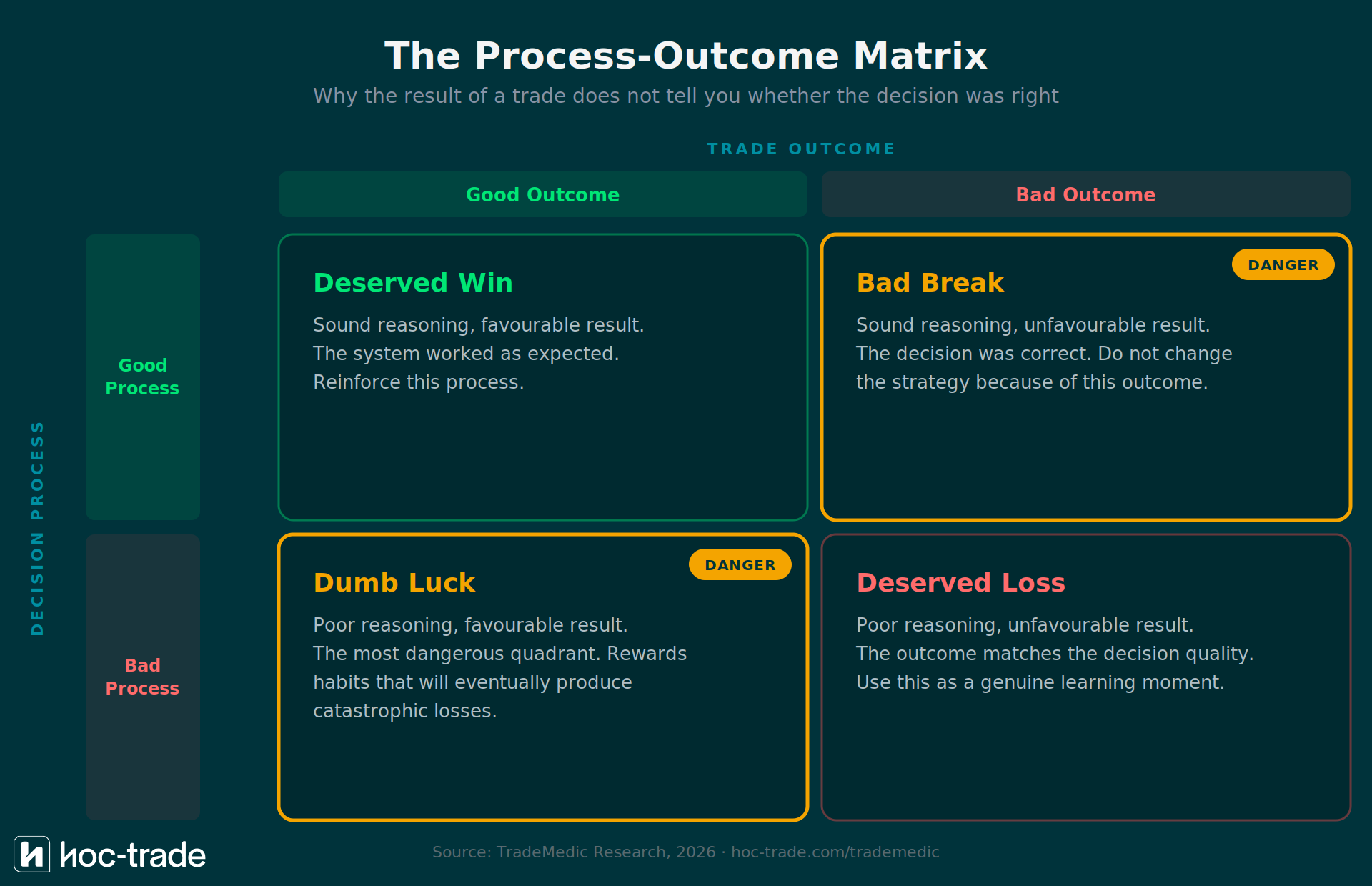

There is a useful framework for thinking about this called the process-outcome matrix. It maps four possible combinations of decision quality and result quality.

A good process with a good outcome is a deserved win. A bad process with a bad outcome is a deserved loss. Both of these are straightforward. The problems come from the other two boxes.

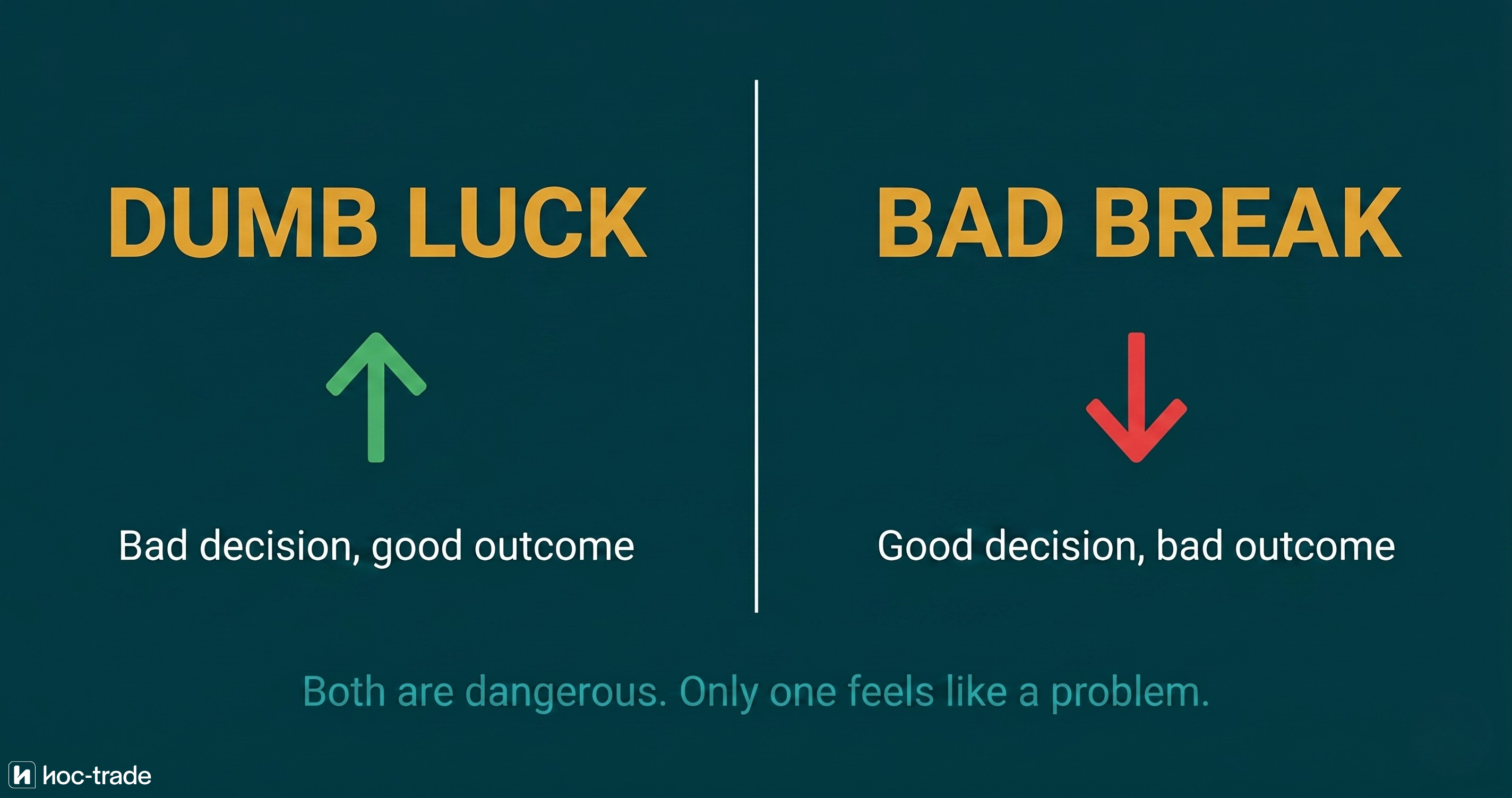

A bad process with a good outcome is dumb luck. The trader did the wrong thing and it worked anyway. A good process with a bad outcome is a bad break. The trader did the right thing and it did not work this time.

Dumb luck is arguably the more dangerous of the two, because it teaches the trader exactly the wrong lesson. It rewards the behaviour the trader should be eliminating. And because the outcome was positive, the trader has no reason to question it. Instead, they believe they have found something that works.

Bad breaks, on the other hand, create doubt where no doubt is warranted. A trader follows their system, takes a loss, and starts wondering whether the system is broken. Over enough bad breaks in a row (which is statistically inevitable over hundreds of trades), the trader abandons a profitable strategy and starts searching for a new one.

How does outcome bias show up in real trading decisions?

Consider a common scenario. A trader holds a position that moves against them on unexpected news. Instead of cutting the loss according to their plan, they add to the position. The price recovers and runs into their original take-profit. The trade closes in profit.

What does the trader take away from this experience? That doubling down works. That trading the bounce after news is a viable strategy. That their instinct to hold through the drawdown was correct. None of these conclusions follow from what actually happened. The trader deviated from their plan, got lucky, and is now treating luck as evidence of skill. The next time a similar situation occurs, they will double down again. And eventually, the recovery will not come.

TradeMedic's data on doubling down tells a clear story here. Only 5% of profitable traders in a dataset of 500,000+ accounts show this pattern among their top issues, compared to roughly 20% of all traders. The math alone explains why: a 50% loss requires a 100% gain just to break even. Traders who double down and survive are experiencing the process-outcome matrix's most dangerous quadrant. They are not learning a strategy. They are rehearsing a habit that will eventually produce a catastrophic loss.

Now consider the opposite situation. A trader opens a position according to their strategy and closes it at the planned take-profit level. Good trade. Good outcome. But the price keeps running. The trader watches what feels like money slipping away and re-enters to capture the remaining move. The price reverses. The second trade wipes out the profit from the first. Frustrated, the trader doubles down to recover at least the original gain. The price keeps falling.

The initial decision to take profit was correct according to the system. But watching the price continue upward created a bad break feeling: the sense that a good decision produced an inferior result. That feeling is outcome bias reframing what was actually a disciplined exit into what feels like a mistake. And the cascade that follows (re-entry, then doubling down, then desperation) is a textbook sequence of increasingly emotional decisions, each one moving further from the original plan.

This connects directly to loss aversion. Research by Kahneman and Tversky on prospect theory showed that losses feel roughly 2.5 times as painful as equivalent gains feel good. When outcome bias makes a trader interpret a missed opportunity as a loss, loss aversion amplifies the emotional response and drives the trader toward increasingly irrational recovery attempts (e.g. revenge trading).

Why is outcome bias particularly dangerous for traders?

Most cognitive biases distort a single decision. Outcome bias distorts the system used to make all future decisions. That is what makes it uniquely destructive.

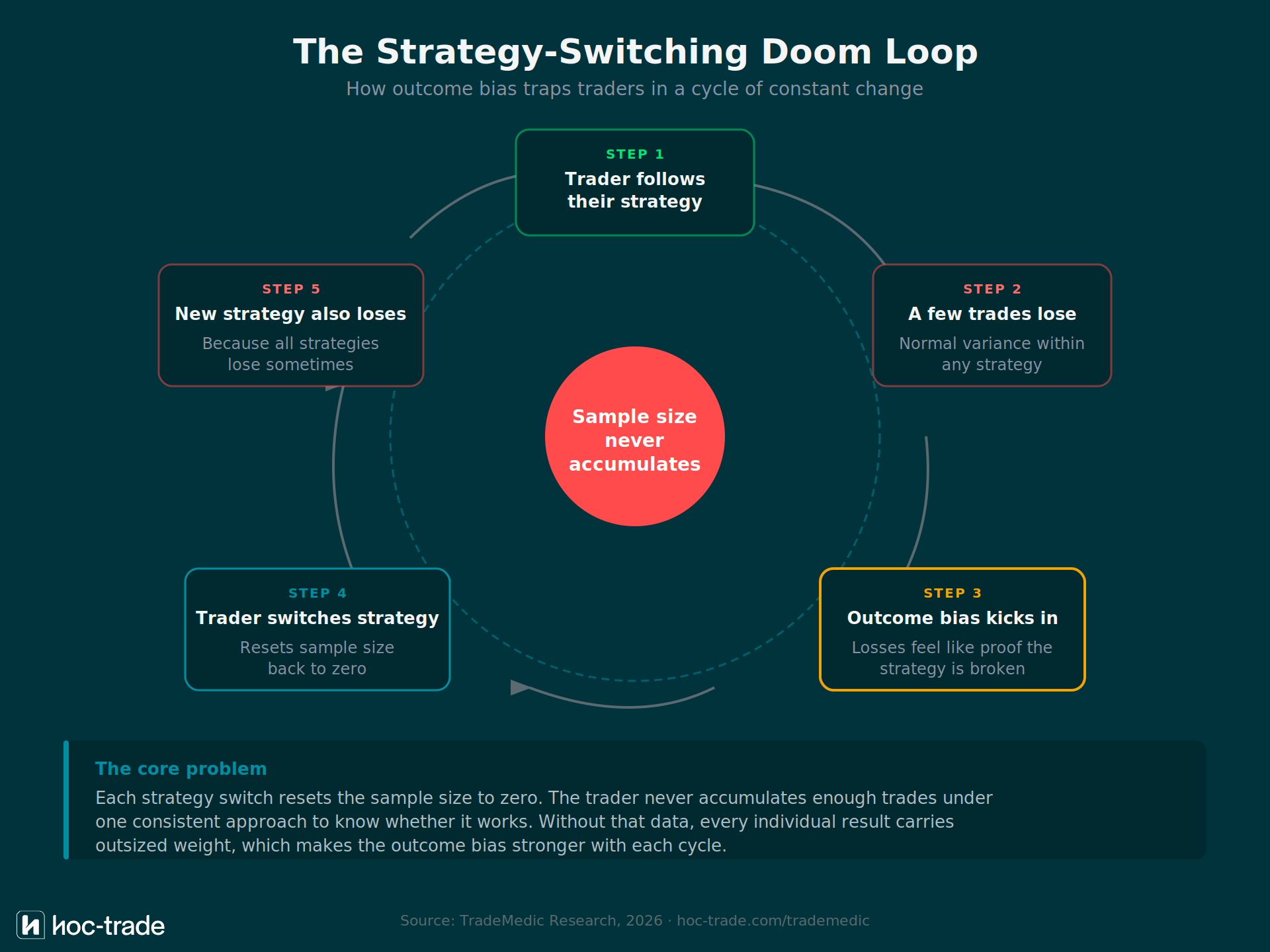

When a trader evaluates trades by their results rather than their process, every loss becomes evidence that the strategy is broken and every win becomes evidence that whatever they did was right. Over time, this produces constant strategy adjustments driven by random variance rather than genuine performance signals. The trader ends up in a loop of switching approaches every few weeks, never staying with any system long enough to evaluate it properly.

The research confirms this is not limited to amateur traders. The NBA coaching study found that even professionals with decades of experience and access to sophisticated performance data were 17% more likely to change their approach after a narrow loss than a narrow win. The difference between a one-point loss and a one-point win is noise, not signal. But the coaches responded as if it were meaningful information. Traders do the same thing. A stop loss gets hit by two pips and the trader concludes their stop placement strategy needs to change. A take-profit is missed by three pips and the trader concludes they should be taking profits earlier.

The longer this cycle runs, the worse it gets. Each strategy change resets the trader's sample size to zero. They never accumulate enough trades under one consistent approach to know whether it works. And without that data, every individual result carries outsized weight in their evaluation, which means the outcome bias gets stronger, not weaker, with each switch. It is a self-reinforcing loop.

How can traders reduce the impact of outcome bias?

The first step is recognising that two things can be true at the same time: a good trade can have a bad outcome, and a bad trade can have a good outcome. This sounds simple. In practice, it is extremely difficult to internalise, because every instinct pushes traders to evaluate decisions by their results. Accepting that a loss can be the correct outcome of a correct decision goes against how most people think about performance.

One practical approach is to separate the evaluation of trade execution from the evaluation of trade results. Before looking at the P&L of a trade, assess whether the entry met your criteria, whether the stop and target were placed according to your plan, and whether you managed the trade according to your rules. Score the process first. Then look at the result. If the process was sound and the result was a loss, that is a bad break, not a bad trade. If the process was poor and the result was a profit, that is dumb luck, not a good trade.

Basketball coaches have started doing something similar. Many now use shot selection grading systems where they evaluate whether a shot was a good decision independently of whether it went in. A wide-open three-pointer that misses is still graded as a good shot decision. A contested fadeaway that happens to drop is still graded as a poor shot decision. The outcome is recorded separately. Over enough games, the process grades become a far better predictor of future performance than the outcome grades.

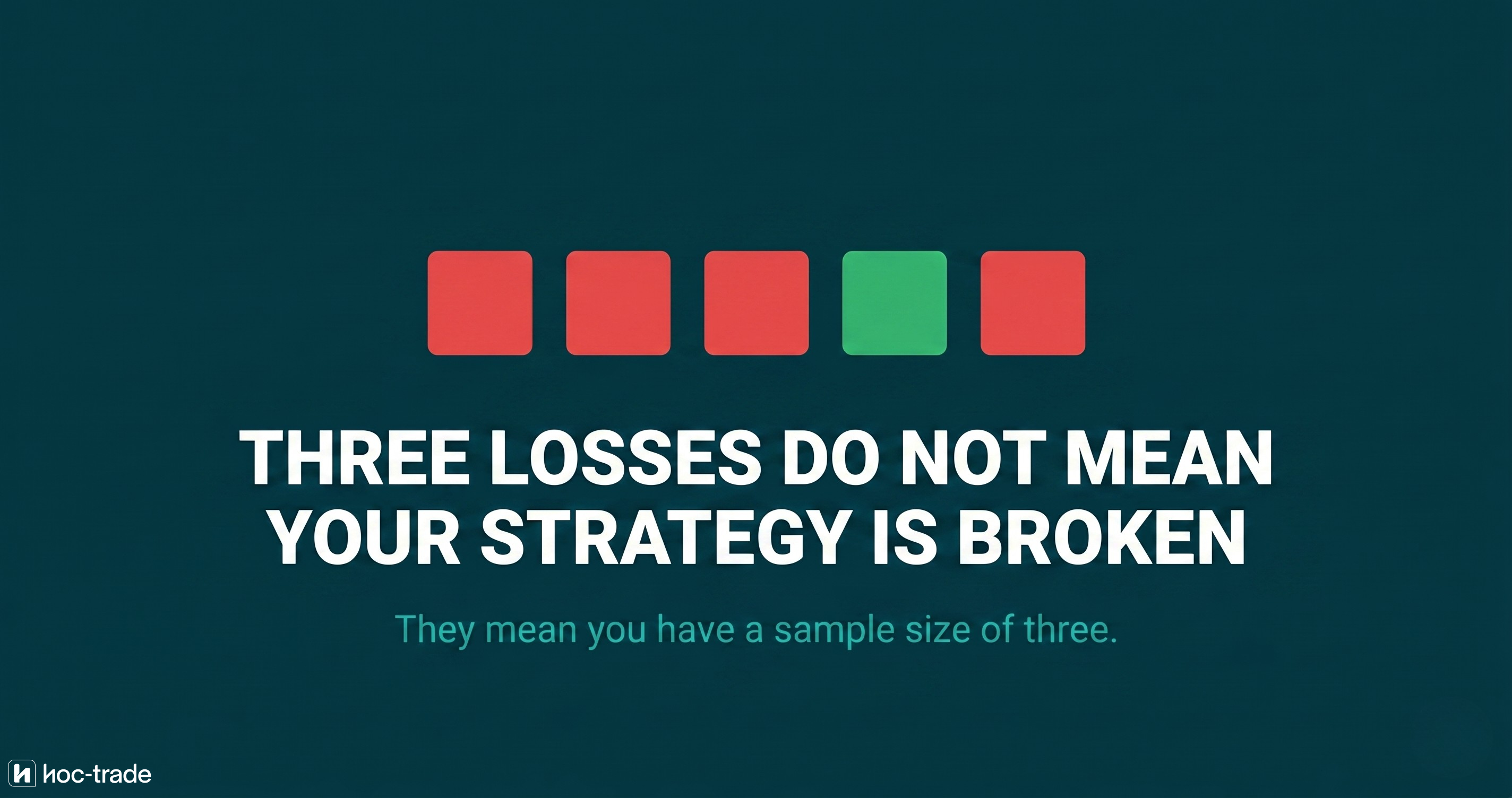

The second defence is sample size. The shorter the evaluation window, the more outcome bias dominates. A trader who evaluates their strategy after five trades is almost entirely at the mercy of variance. A trader who evaluates after two hundred trades is working with a signal that actually means something. The discipline to wait for statistical significance before adjusting a strategy is one of the hardest things in trading, but it is also one of the most important.

Reducing complexity during trading sessions also helps. Every additional variable (more screens, more symbols, more news feeds, more open positions) compresses the time available for each decision. When decision time is short, the brain defaults to the fastest available shortcut. And the fastest shortcut for evaluating a trading decision is looking at the last result. Narrowing focus to fewer instruments and simpler setups gives the brain more space to evaluate decisions on their own terms rather than by their most recent outcome. Lastly, reducing the risk per trade helps overcoming outcome bias. If we feel a loss streak of 5 or 10 trades already severely damages our overall performance, we are much more likely to take action and change our strategy, even though we may have only had some back luck. Traders with an average risk per trade of <0.5% shows to be profitable >60% more often than traders with a risk of 1-2% per trade.

What does the data show about outcome bias in trading?

Outcome bias is not a pattern that TradeMedic detects directly as a single metric. It is the underlying driver behind several patterns that are directly measurable in trading data. When a trader doubles down on a losing position because a previous double-down happened to work out, that is outcome bias feeding into the doubling down pattern. When a trader abandons a strategy after a string of losses that fall within normal variance, that is outcome bias feeding into inconsistent execution.

Across a dataset of 500,000+ trader accounts, TradeMedic detects 60+ behavioural patterns and calculates each trader's personal performance impact for every one of them. The pattern most closely linked to outcome bias is doubling down, where only 5% of profitable traders show it versus roughly 20% overall. Overtrading is another: the compulsive need to "make it back" after a loss drives excessive trading activity, and TradeMedic's data shows that loss-making traders are more than twice as likely to show overtrading as profitable ones.

What makes behavioural data valuable for overcoming outcome bias is that it evaluates patterns across hundreds or thousands of trades, not individual results. A trader who thinks their strategy is failing because of three recent losses can look at their data across the full history and see whether those losses are noise or signal. That is the difference between reacting to outcomes and understanding your actual performance.

The trade that felt right is not always the trade that was right

Outcome bias is uncomfortable to confront because it challenges the most natural feedback loop in trading: you made money, therefore you did the right thing. Pulling that apart and asking whether the decision was actually sound regardless of the result requires a kind of intellectual honesty that most traders never practise. It also requires enough data to distinguish luck from skill, which is impossible to do from individual trade results alone.

The traders who perform well over long periods are not the ones who made the most profitable individual trades. They are the ones who ran the best process consistently and let the probabilities work over large sample sizes. Every time a trader changes their strategy because it "stopped working" after a few losing trades, they are resetting that sample size and starting over. Outcome bias is the reason most traders never accumulate enough consistency to know whether their approach actually works.