Loss Aversion in Trading: Why You Hold Losers and Cut Winners Short

Every trader knows the rule: cut your losses early, let your profits run. It sounds simple. In practice, most traders do the opposite. They hold losing trades far too long, hoping for a recovery that rarely comes, and close winning trades too early, locking in small gains while leaving larger profits on the table.

This isn't a discipline problem. Or rather, discipline is part of it, but the pattern runs deeper than willpower. In 1979, two psychologists, Daniel Kahneman and Amos Tversky, published a paper that would eventually earn Kahneman a Nobel Prize in Economics. They called it Prospect Theory, and it explains precisely why traders behave this way, even when they know better.

The short version: losing hurts roughly two to three times more than winning feels good. That asymmetry distorts every trading decision you make, from where you set your stop loss to when you take profit. Understanding how it works is the first step toward trading against your own worst instincts.

What is loss aversion and how does Prospect Theory explain it?

Loss aversion is the human tendency to feel the pain of a loss more intensely than the pleasure of an equivalent gain. Kahneman and Tversky demonstrated this through a series of experiments that revealed a consistent pattern in how people evaluate risk.

Their most famous experiment presented participants with two separate choices. In the first, participants chose between a guaranteed loss of $3,000 or an 80% chance of losing $4,000 with a 20% chance of losing nothing. In the second, they chose between a guaranteed gain of $3,000 or an 80% chance of winning $4,000 with a 20% chance of winning nothing.

The results were striking. When facing losses, 92% of participants chose the gamble, preferring to risk a larger loss for a chance to avoid losing anything. When facing gains, the pattern reversed. Only 20% took the gamble. The vast majority preferred the smaller guaranteed win.

Both gambles carried similar expected values. But people treated them completely differently depending on whether money was being gained or lost. When gains are on the table, we play it safe. When losses are on the table, we gamble. That asymmetry is loss aversion in action, and it shapes trading behaviour in ways most traders never recognise.

The exact strength of loss aversion has been debated in academic circles, and some researchers argue it's more context-dependent than originally claimed. But in trading specifically, the evidence is consistent: across large datasets of real trades, the pattern shows up regardless of market, asset class, or experience level. (See the research section at the end of this article for details.)

How does loss aversion affect trading decisions?

Loss aversion creates two destructive patterns that feed off each other. On the loss side, traders take on additional risk to avoid realising a loss. On the profit side, they rush to lock in gains before they can disappear. The combination is toxic: small wins and large losses, repeated over hundreds of trades.

This combined pattern has a name in behavioural finance: the disposition effect. It describes the tendency to sell winners too early and ride losers too long. It's been measured directly in brokerage account data, where studies of tens of thousands of real investors found that the winning stocks people sold continued to outperform the losing stocks they kept. The pattern held even after controlling for tax considerations, portfolio rebalancing, and transaction costs. The disposition effect isn't just a bias. It's a measurable drag on returns. (More on this research below.)

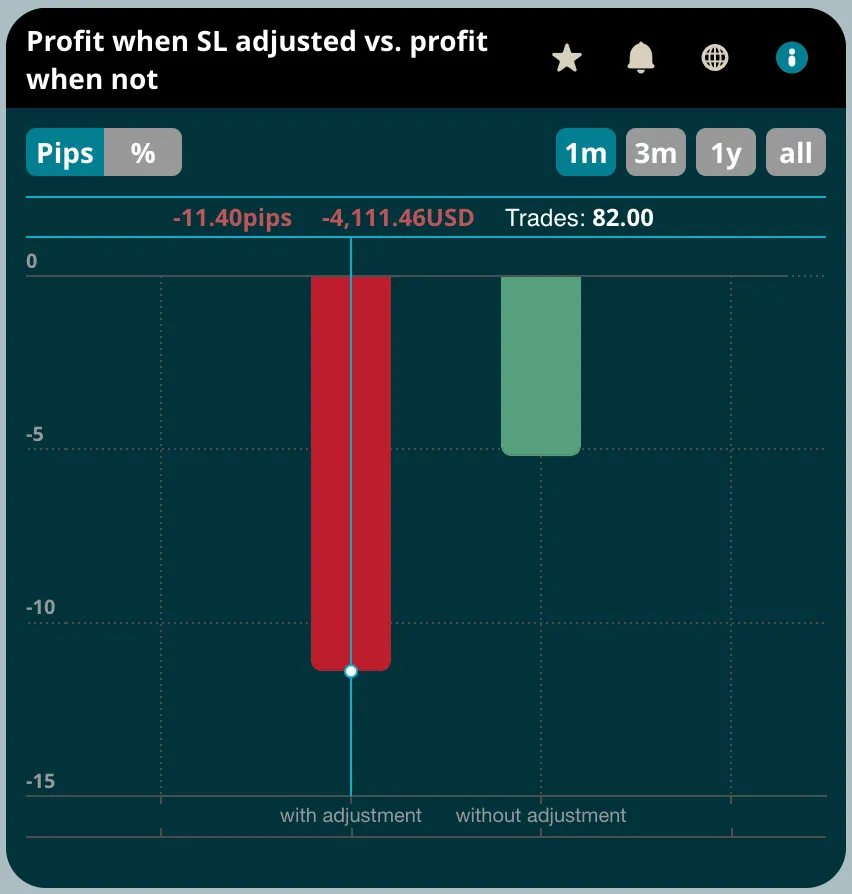

The loss side. A trader enters a position with a stop loss set at a reasonable level. The trade moves against them. Instead of accepting the loss and moving on, they move their stop loss further away, giving the trade "more room." What they're really doing is gambling, exactly like the 92% of participants in Kahneman and Tversky's experiment who chose the risky option to avoid a guaranteed loss. In trading terms, this means letting a manageable $500 loss become a $2,000 loss because closing the position at $500 felt worse than the uncertain possibility of recovery.

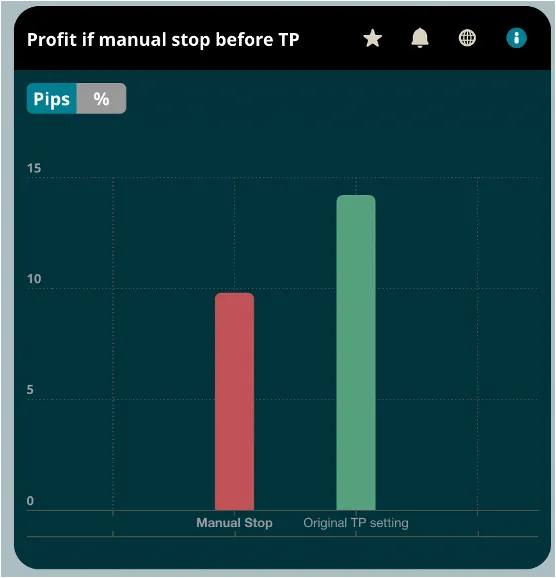

The profit side. A trader enters a position with a take profit target of $2,000. The trade moves in their favour and reaches $1,000 in unrealised profit. At this point, the fear of watching that $1,000 disappear becomes overwhelming. They close the trade manually, securing the smaller gain. This mirrors the 80% of experiment participants who chose the guaranteed $3,000 over the chance at $4,000. The potential regret of watching profits vanish outweighs the potential reward of letting the trade reach its target.

Over time, these two behaviours compound. Losses grow larger than they should be. Profits stay smaller than they could be. The trader's overall expectancy deteriorates even if their trade selection and timing are sound.

Professional traders show the same pattern, though to a lesser degree. Research on futures traders found that all of them held losers longer than winners, but the least successful held losers the longest, while the most successful cut them the fastest. The difference isn't the absence of loss aversion. It's how quickly you act against it.

Why do traders keep adjusting their stop loss?

Stop loss adjustment is one of the clearest fingerprints of loss aversion in trading data. A trader sets a stop loss at the point where their trade thesis is invalidated. The market moves toward that level. Rather than letting the stop trigger, the trader widens it, sometimes repeatedly. Sometimes even adds another position to the loss trade (Dollar Cost Averaging or DCAing).

This behaviour feels rational in the moment. The trader tells themselves the market is about to reverse, or that the original stop was too tight, or that giving it "a little more room" is prudent risk management. But the underlying driver is almost always the same: the pain of crystallising a loss feels worse than the uncertainty of staying in the trade.

Kahneman and Tversky's research explains why. In the loss domain, people become risk-seeking rather than risk-averse. A guaranteed loss (hitting the stop) is psychologically more painful than an uncertain outcome (widening the stop and hoping), even when the uncertain outcome carries a higher expected loss. The trader's brain is running the same calculation as the experiment participants: given a choice between a certain loss and a gamble, take the gamble.

The data confirms this matters. Across trading accounts, trades where the stop loss was adjusted further away from the entry price consistently underperform trades where the original stop was left in place. The "extra room" that feels like it should help almost always makes things worse.

Why do traders close winning trades too early?

The flip side of loss aversion is equally damaging but harder to recognise because it feels like good decision-making. Closing a winning trade early feels responsible. You've secured a profit. You've "taken money off the table." The problem is that this behaviour, repeated over hundreds of trades, systematically caps your upside while your losses remain uncapped by the stop loss adjustments described above.

Prospect Theory explains the mechanism clearly. In the gain domain, people are risk-averse. How often have you heard already: “you never go broke taking a profit”?. A trader sitting on $1,000 of unrealised profit experiences that gain as something they already possess. Letting the trade continue toward a $2,000 target means risking what they "have" for something they don't yet. The fear of giving back the unrealised profit triggers the same loss aversion that distorts the losing side of the equation.

This is why the common advice to "let your winners run" is so difficult to follow in practice. It's not that traders don't understand the logic. The problem is that their emotional circuitry treats unrealised profit as something that can be lost, and the prospect of that loss feels disproportionately painful compared to the potential of additional gain.

What happens in the brain when you're about to take a loss?

Neuroscience has moved loss aversion beyond theory. Brain imaging studies show that the amygdala, a structure involved in threat detection, fires in response to prospective losses and sends signals to the brain's value-processing regions before the prefrontal cortex, the part responsible for rational analysis, has finished evaluating the situation. The emotional alarm arrives first. This is why traders so often "know" they should cut a loss but find themselves unable to do it in the moment. The decision feels like a willpower failure, but it's a timing problem: the threat response is faster than the analytical one.

The same research points toward a solution. Studies testing cognitive reappraisal strategies, specifically reframing each decision as one of many in a portfolio rather than treating it as an isolated event, found that this reduced both loss-averse behaviour and the physiological arousal associated with losses. The mechanism works by engaging the prefrontal cortex to dampen the amygdala's threat signal. This has a direct connection to the countermeasures below: thinking in risk units rather than dollar amounts isn't just a mental trick. It activates the exact neural pathway that reduces loss aversion at its source.

What other trading behaviours does loss aversion drive?

Stop loss adjustment and premature profit-taking are the two most visible expressions of loss aversion in trading, but the bias ripples through several other patterns.

Revenge trading

After a loss, traders often re-enter the market immediately, trying to recover what they just lost. The pain of the loss creates urgency to "fix" it. This leads to impulsive trades taken without proper setups, and the resulting losses compound the original damage. TradeMedic™ data shows revenge trading is the second most common improvement opportunity across 500,000+ accounts, affecting 40% of all traders.

Doubling down

Rather than closing a losing position, some traders add to it, averaging down their entry price. The logic feels sound: if the asset was a good buy at $100, it's an even better buy at $80. But the underlying motivation is often loss aversion. Accepting the loss at $100 is painful, so the trader increases their exposure to avoid it, magnifying the eventual loss if the position continues to move against them.

Failing to cut losses entirely

Some traders don't just widen their stops. They remove them. A position that was meant to risk 1% of their account now has no exit plan at all, because every potential closing price represents a realised loss that the trader's brain desperately wants to avoid.

Fighting the trend

Loss aversion can keep traders anchored to a directional bias long after the market has moved against it. Admitting the original thesis was wrong means accepting a loss, so the trader holds the position or adds to it, hoping the trend will reverse.

The endowment effect

Closely related to loss aversion, this is the tendency to overvalue something simply because you own it. In trading, it shows up as irrational attachment to open positions. A trader who would never enter a particular trade at its current price may still refuse to close it, because selling feels like giving up something they possess.

Each of these behaviours has its own dynamics, but loss aversion is the common thread. The pain of realising a loss is the psychological trigger that sets the destructive cycle in motion.

How to overcome loss aversion in trading

Loss aversion is a deeply wired human tendency. You can't eliminate it. But you can build systems that prevent it from distorting your trading decisions. Three approaches have shown consistent results across traders.

Reframe how you measure trades. Much of loss aversion's power comes from how we value money. A $2,000 loss hurts viscerally because $2,000 is real, tangible, and personal. One effective counter is to stop thinking in currency terms entirely. Instead, measure trades in units of risk ("R"). If your planned risk on a trade is $500, that's 1R. A $2,000 loss is 4R. A $1,500 gain is 3R. By abstracting away from dollar values, you reduce the emotional charge that triggers loss-averse behaviour. As mentioned in the neuroscience section, this kind of reframing engages the prefrontal cortex and dampens the amygdala's threat response. It's not just a mindset shift. It changes how your brain processes the decision.

Automate your exits. The most reliable way to prevent stop loss adjustment is to remove the option. Set your stop loss and take profit when you enter the trade, then walk away. If your trading platform allows it, use bracket orders that close the position automatically at either level. You can't adjust a stop loss if you're not watching the screen. This doesn't require willpower. It requires a process that takes the decision out of your hands during the moment when your brain is least equipped to make it rationally. The amygdala's influence peaks in the moment of decision, when a loss is staring you in the face. Pre-committing to exit levels sidesteps that moment entirely.

Use your own data to build awareness. Awareness alone doesn't fix loss aversion, but it creates the foundation for every other fix. When you can see, in your own trading history, how much stop loss adjustments have cost you or how much additional profit you left on the table by closing early, the abstract concept becomes personal and concrete. Tools like TradeMedic™ AI screen for exactly these behaviours across your trade history and calculate the personal cost in dollar terms. That kind of specificity is what turns "I should stop doing this" into "this has cost me $4,700 in the last three months, and here are the 12 trades where it happened." The gap between knowing about loss aversion in the abstract and seeing its cost in your own trades is the gap between understanding a concept and changing a behaviour.

What does TradeMedic data show about loss aversion in trading?

TradeMedic™ AI analyses over 500,000 trader accounts for 60+ behavioural patterns, several of which map directly to loss aversion. Premature profit-taking, stop loss adjustment, revenge trading, doubling down, and failure to cut losses all carry detectable signatures in trade data.

Each trader who connects their account receives a personalised breakdown of how these behaviours affect their own performance, with specific dollar amounts and trade examples. A detailed data analysis of each loss-aversion-related pattern is available in the individual pattern articles linked below.

Source: TradeMedic Research, 2026

How does TradeMedic AI detect loss aversion patterns?

TradeMedic™ AI doesn't look for "loss aversion" as a single pattern. Instead, it identifies the specific trading behaviours that loss aversion produces. Each behaviour has a distinct data fingerprint.

For stop loss adjustment, the system compares the original stop loss level at trade entry with the final stop loss level at trade close. When the stop was moved further from entry on a losing trade, the system flags it and calculates what the trade outcome would have been if the original stop had been left in place.

For premature profit-taking, the system identifies trades that were manually closed in profit before reaching the original take profit target. It then simulates what would have happened if the trade had been allowed to run to the original target, calculating the difference.

For revenge trading, the system analyses the timing between a losing trade's close and the next trade's open. Trades entered within the personal dangerous window after a loss are flagged and their performance is compared against the trader's baseline.

Each of these detections feeds into the trader's personalised report, showing not just whether the behaviour exists but how much it's costing them in real terms. That level of specificity is what makes the difference between knowing about loss aversion and doing something about it.

The bottom line

Loss aversion is not a flaw in your character. It's a feature of human psychology that served our ancestors well but works against us in trading. The asymmetry Kahneman and Tversky identified, that losses feel two to three times more painful than equivalent gains feel good, is present in every trader's decision-making. The question isn't whether it affects you. It's how much it's costing you.

The traders who manage it best aren't the ones with the most discipline. They're the ones who build systems that account for the bias: automated exits, risk-based measurement, and data-driven awareness of their own patterns. The bias doesn't disappear. The damage it does can.

Research behind this article

This section collects the academic studies referenced throughout the article. Each finding above is drawn from peer-reviewed research. Traders interested in the evidence base can explore these sources further.

Prospect Theory (1979). Daniel Kahneman and Amos Tversky, "Prospect Theory: An Analysis of Decision Under Risk," Econometrica 47(2): 263-291. The foundational paper establishing that people are risk-averse in gains and risk-seeking in losses, and that losses carry roughly 2-2.5x the psychological weight of equivalent gains. Referenced for Kahneman's 2002 Nobel Prize in Economics.

The Disposition Effect (1985). Hersh Shefrin and Meir Statman, "The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence," The Journal of Finance 40(3): 777-790. Coined the term "disposition effect" and proposed it was driven by a combination of prospect theory, mental accounting, regret aversion, and self-control problems. One of the most cited papers in behavioural finance.

Brokerage Account Evidence (1998). Terrance Odean, "Are Investors Reluctant to Realize Their Losses?" The Journal of Finance 53(5): 1775-1798. Analysed 10,000 accounts at a large US discount brokerage and found a strong preference for selling winners over losers. Winning stocks that investors sold outperformed losing stocks they kept by 3.4% over the following year. The effect was not explained by tax-loss harvesting, rebalancing, or transaction costs.

Cross-Cultural Replication (2007). Chen, Kim, Nofsinger, and Rui analysed almost 50,000 Chinese investors using brokerage data (1998-2002) and found they were 67% more likely to sell a winner than a loser. Confirms the disposition effect is not limited to US markets.

Large-Scale Online Trading Data (2014). Liu et al., "Prospect Theory for Online Financial Trading," PLOS One 9(10). Analysed 28.5 million trades from 81,300 traders on an online social trading platform over 28 months. Found clear evidence of both the reflection effect (risk-seeking in losses, risk-averse in gains) and loss aversion in real trading data at unprecedented scale.

Professional Traders (2000). Locke and Mann, "Do Professional Traders Exhibit Loss Realization Aversion?" Studied professional floor futures traders and found that while all traders held losers longer than winners, the least successful traders held losers the longest and the most successful cut them fastest. Experience reduces but does not eliminate the bias.

Amygdala and Loss Aversion (2010). De Martino, Camerer, and Adolphs, "Amygdala Damage Eliminates Monetary Loss Aversion," PNAS 107(8): 3788-3792. Patients with bilateral amygdala damage showed dramatically reduced loss aversion. The amygdala generates an anticipatory response to prospective loss, conveyed to value-processing regions (ventral striatum, orbitofrontal cortex), biasing decisions before rational analysis completes.

Neural Correlates of Loss Aversion (2013). Sokol-Hessner, Camerer, and Phelps, "Emotion Regulation Reduces Loss Aversion and Decreases Amygdala Responses to Losses," Social Cognitive and Affective Neuroscience 8(3): 341-350. fMRI study showing behavioural loss aversion correlated with amygdala activation. Cognitive reappraisal strategies reduced both loss aversion and amygdala responses to losses, with increased activity in dorsolateral and ventromedial prefrontal cortex.

"Thinking Like a Trader" (2009). Sokol-Hessner et al., "Thinking Like a Trader Selectively Reduces Individuals' Loss Aversion," PNAS 106(13): 5035-5040. A perspective-taking strategy that reframed individual decisions as part of a portfolio reduced both behavioural loss aversion and skin conductance responses to losses. The effect was driven by dampening arousal to losses specifically, not increasing arousal to gains.

The Academic Debate (2018-2024). Gal and Rucker, "The Loss of Loss Aversion," Journal of Consumer Psychology 28(3): 497-516 (2018), argued the evidence for universal loss aversion is weaker than assumed. Mrkva et al. (2020) responded that loss aversion has moderators but "reports of its death are greatly exaggerated." A 2024 meta-analysis by Brown, Imai, Vieider, and Camerer across 607 estimates from 150 studies found robust evidence for loss aversion. The consensus: the effect is real and significant, though its magnitude varies by context.