Pessimism Bias in Trading: Why Traders Close Winning Trades Too Early

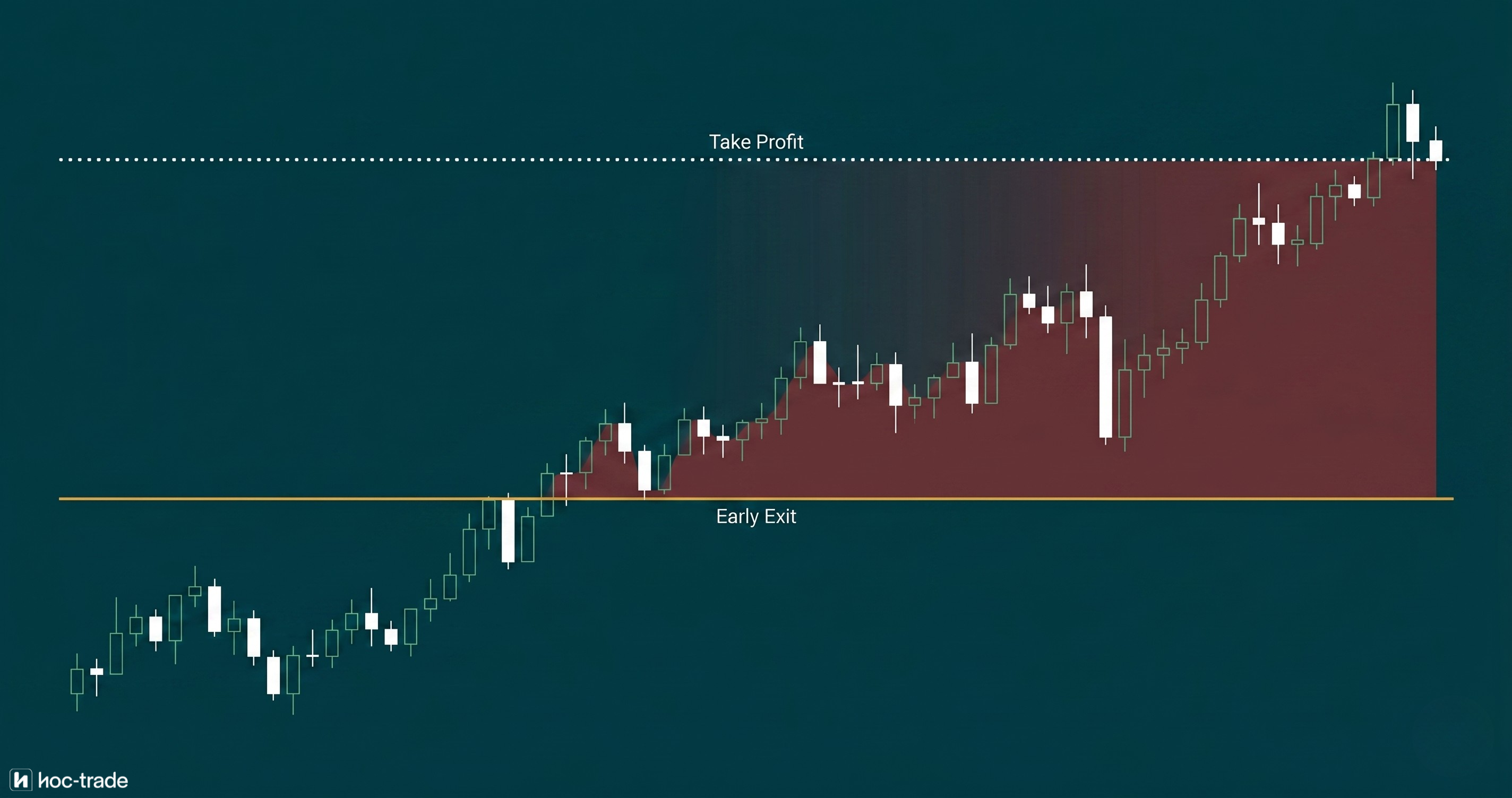

The trade is in profit. Your take-profit level is 40 pips away and the price is moving in your direction. Everything about the setup is working. And then a small pullback appears on the chart. Nothing unusual. Normal price action. But something shifts. You start watching the unrealised profit number instead of the chart. You think about the last time a trade reversed on you from this exact kind of position. You close the trade manually. Ten pips of profit instead of forty.

The price keeps running. It hits your original take-profit level an hour later. You stare at the screen knowing you left thirty pips on the table because a pullback that meant nothing felt like the start of a reversal.

This is not a discipline failure. This is the pessimism bias at work. It is a well-documented cognitive tendency to overestimate the probability of negative outcomes and underestimate the probability of positive ones. In trading, it shows up most clearly in how traders manage their winning trades. And the cost, over hundreds of trades, is enormous.

What is the pessimism bias?

The pessimism bias is the tendency to overweight the likelihood of negative events happening and underweight the likelihood of positive events. It is closely related to the negativity bias, which describes the brain's broader tendency to process negative information more intensely than positive information of equal magnitude.

The neuroscience behind this is well established. The amygdala, the brain's threat-detection centre, uses roughly two-thirds of its neurons to detect negativity. Brain imaging studies show that negative stimuli activate the amygdala within milliseconds, while positive stimuli require more time and conscious processing to generate a comparable response. Negative images produce approximately twice the neural response compared to neutral ones. The brain is not wired to treat good news and bad news equally. It is wired to treat bad news as urgent and good news as optional.

This is an evolutionary feature, not a bug. For most of human history, the cost of missing a threat was death. The cost of missing an opportunity was a smaller meal. The brain evolved to prioritise threats because the downside of ignoring danger was far greater than the downside of ignoring good fortune. But in trading, this asymmetry works against you. The threat is not a predator. The threat is a price reversal. And the brain responds to the possibility of losing unrealised profit with the same urgency it would apply to a physical danger.

One experiment demonstrated this clearly. Participants were given 10 coin flips with a reward of 10 USD for each heads result. When asked how many times they expected to win, the mathematically correct answer is 5. The 1,500 participants averaged 3.9. They systematically discounted the probability of a favourable outcome by over 20%, even in a scenario with clearly defined 50/50 odds. In trading, where probabilities are far less transparent, this discounting effect is even stronger.

Why do traders close winning trades too early?

Every trader learns the rule early: cut your losses and let your profits run. Warren Buffett framed the profit side simply: when it's raining gold, reach for a bucket, not a thimble. The logic is obvious. If your average loss is larger than your average win, you need a win rate well above 50% just to break even. Letting winners run is not optional. It is arithmetic.

And yet most traders do the opposite. They close winning trades early and let losing trades run. This pattern is so consistent that it has its own name in academic literature: the disposition effect. Terrance Odean, studying 10,000 retail brokerage accounts and over 162,000 trades between 1987 and 1993, found that investors sold their winning positions at roughly 1.5 times the rate of their losing positions. The winners they sold went on to outperform the losers they kept by 3.4 percentage points over the following twelve months. Applied to the roughly 3 trillion USD in U.S. retail-held equities at the time, the implied annual wealth destruction from premature winner-selling exceeded 100 billion USD.

Pessimism bias is one of the key psychological drivers behind this pattern. When a trade is in profit, the trader's brain does not treat the current gain as progress toward the target. It treats it as something that could be taken away. The amygdala flags the possibility of reversal as a threat. The trader overestimates the probability of the price turning against them and underestimates the probability of the trade reaching the take-profit. The result is a manual close at a fraction of the intended target.

This connects directly to loss aversion. Research by Kahneman and Tversky on prospect theory showed that losses feel roughly 2.5 times as painful as equivalent gains feel good. The value function is steeper for losses than for gains, which means the pain of watching a profitable trade reverse and turn into a loss is felt far more intensely than the pleasure of watching it continue to grow. Pessimism bias amplifies this: it tells the trader that the reversal is more likely than it actually is, and loss aversion makes the potential pain of that reversal feel disproportionately severe. Together, they create an almost irresistible urge to close early.

How does the pessimism bias get worse after a losing trade?

Pessimism bias is not constant. It is situational. Research has shown that depressive symptoms explain 34 to 45% of the variance in negative self-referent processing. People in a negative emotional state make more pessimistic probability estimates than people in a neutral state. In trading, the most reliable trigger for a negative emotional state is a losing trade.

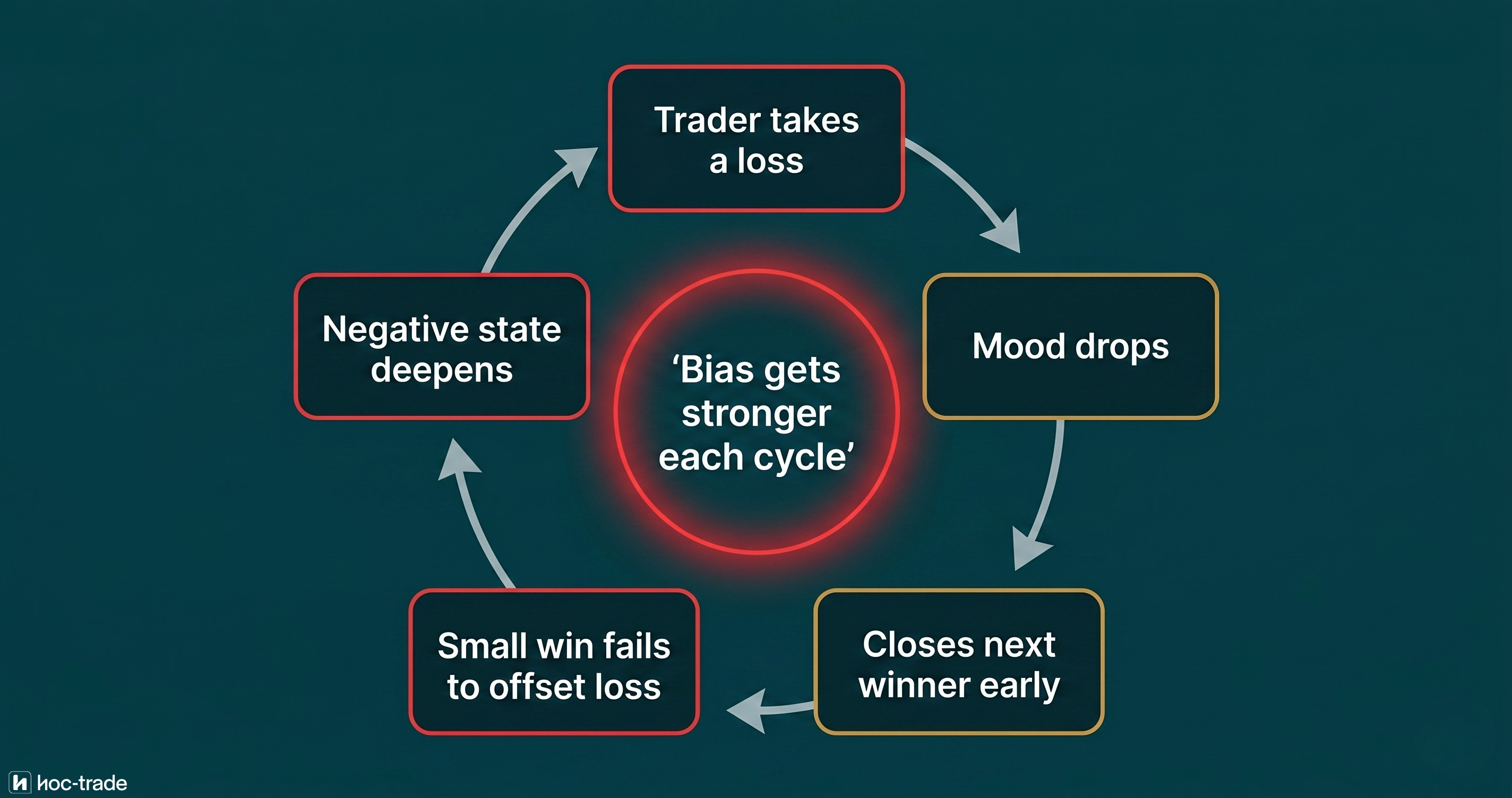

This creates a compounding cycle. A trader takes a loss. Their mood drops. On the very next trade, their pessimism bias is now stronger than usual. They enter a position, it moves into profit, and the urge to close early is even more intense than it would be on a normal day. They close early, take a small win that does not offset the previous loss, and their net position for the day is still negative. That leaves the trader with an unhealthy reward risk balance and reinforces the negative emotional state, which makes the pessimism bias even stronger on the following trade.

TradeMedic's analysis of cutting profits early includes exactly this dimension. The system does not just detect whether a trader would have been better off not closing profit trades manually. It also tracks whether the probability of manually closing a profit trade increases after the trader had a loss trade beforehand. For many traders, the data shows a clear spike: the likelihood of cutting a winner short rises significantly when the previous trade was a loss. The pessimism bias becomes measurable in the trading data.

Does pessimism bias only affect how traders take profits?

The Medium article this was originally based on focused entirely on profit-taking. But the data tells a more complete story. Pessimism bias does not just affect the profit side of a trade. It also distorts how traders set their stop losses.

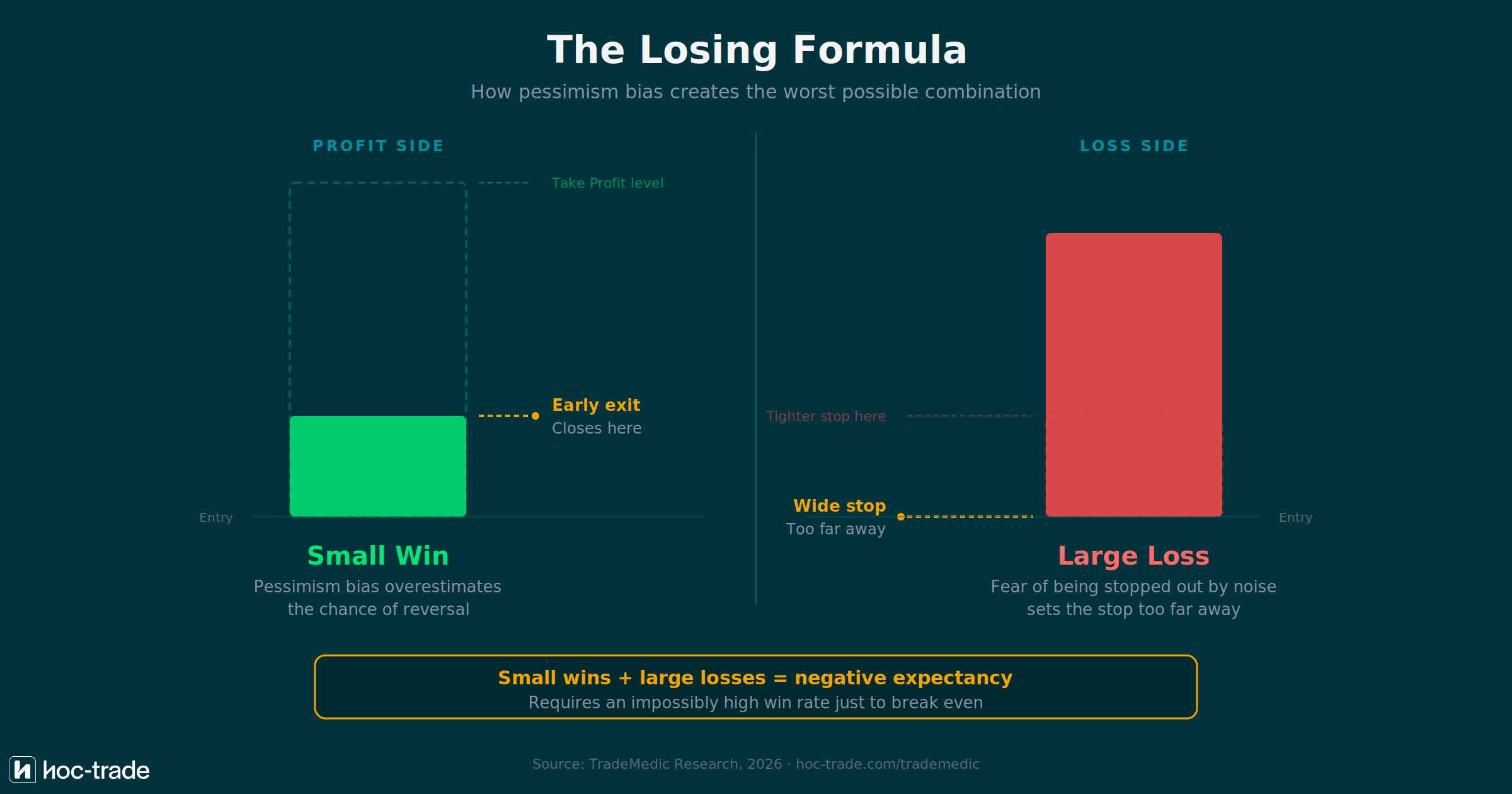

Consider the logic. A pessimistic trader overestimates the probability of the market moving against them. On the profit side, this means closing early because a reversal feels imminent. On the loss side, the same bias should logically produce overly tight stops: if you expect the worst, you protect yourself as tightly as possible.

But that is not what the data shows. Across 500,000+ trader accounts, TradeMedic finds that 5.9% of traders have too-wide stops among their top 5 improvement areas, while only 0.2% show too-tight stops. That is a 30:1 ratio. Traders overwhelmingly err on the side of setting stops too far away, not too close.

This seems to contradict pessimism bias at first glance. But it makes sense when you consider what the trader is actually pessimistic about. They are not pessimistic about the trade direction. They are pessimistic about their stop placement. They remember the trades where their stop was hit by a few pips of noise and the price then moved in their favour. That memory is vivid and painful. So they set their stops wider to avoid reliving it. The handbook describes this precisely: traders with too-wide stops "overestimate the noise in the market" and "tend rather remember painful events, such as trades in which their SL was just hit."

The result is the worst possible combination. Pessimism bias makes the trader close winning trades early (small profits) while simultaneously setting stops too wide (large losses when trades fail). This is the formula for a negative expectancy: your average win is small and your average loss is large. You need an extraordinarily high win rate just to break even, and most traders do not have one.

This connects directly to reward-risk imbalance, one of the patterns TradeMedic detects. When a trader's average win is consistently smaller than their average loss, the system flags this as a structural problem in how the trader manages trades. The pessimism bias article explains the psychology behind why this imbalance develops. The reward-risk imbalance detection shows the trader exactly how much it is costing them.

Can optimism and pessimism bias coexist in the same trader?

Yes. And the data suggests they do. TradeMedic also detects a pattern called overoptimism, where traders set take-profit targets that are unrealistically far from entry. The system simulates closer take-profit levels and finds that performance would improve. This is the optimism bias applied to profit targets: the trader overestimates the probability of price reaching an ambitious level.

8% of all traders show overoptimism in their top 5 improvement areas. Among profitable traders, the figure is 10%. Among loss-making traders, 7%. This means a meaningful number of traders are simultaneously too optimistic about where price will go (setting ambitious TPs) and too pessimistic about whether it will get there (closing manually before the TP is reached). They set a target of 80 pips, then close at 15 because it feels like the reversal is coming.

This is not contradictory. It reflects how different emotional states dominate at different moments in a trade. When setting up the trade, the trader is in a planning state. Optimism is easy. When managing the trade with real money at risk, the amygdala takes over. Pessimism dominates. The same trader can be two different decision-makers at different stages of the same trade.

How to let your profits run without ignoring risk

The first thing to understand is that pessimism bias is not something you can simply decide to stop doing. The amygdala processes threats before conscious thought has time to intervene. By the time you are aware that you feel anxious about a trade reversing, the emotional response has already started influencing your decision-making. The goal is not to eliminate the bias. It is to build systems that reduce its impact on your actual trading behaviour.

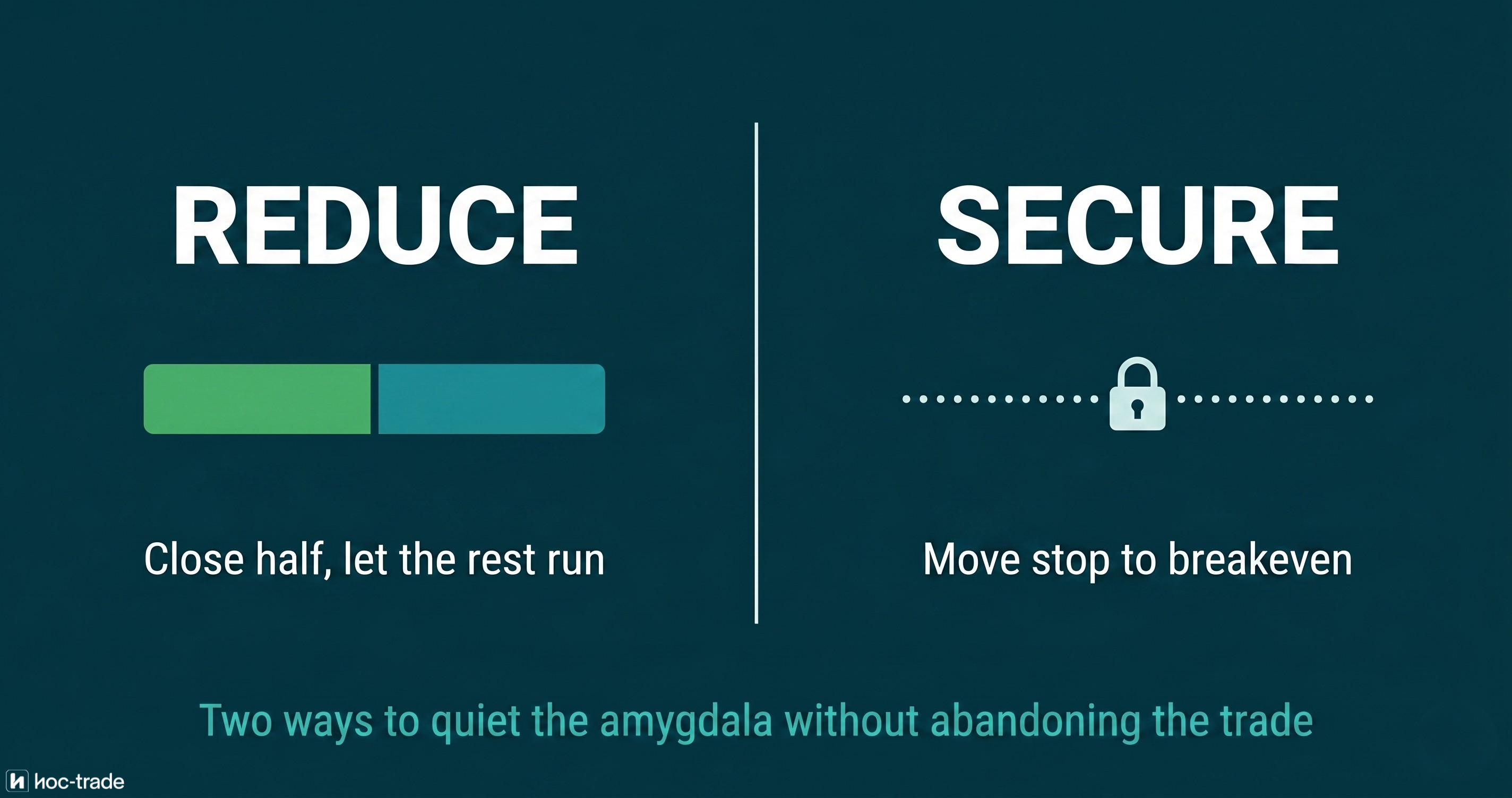

One approach that many traders find effective is to reduce position size rather than close entirely. When the urge to close a profitable trade hits, closing half the position satisfies the psychological need to lock in some profit while leaving the other half to run toward the target. Over time, the trader sees what happened to the remaining half, which builds a personal dataset of evidence that not every pullback turns into a reversal. This is not a complete solution, but it is a meaningful step toward retraining the brain's probability estimates.

A second technique is to move the stop loss to breakeven once the trade reaches a certain profit level, instead of closing it. This removes the possibility of a loss entirely. The trader can no longer lose money on this trade. For many people, this is enough to quiet the amygdala and allow the trade to breathe. TradeMedic's failed de-risking analysis calculates the exact profit level at which each individual trader would benefit most from moving their stop to breakeven. For one trader it might be 10 pips. For another, 25. The optimal level depends on the trader's specific instruments, strategy, and historical trade data.

The third countermeasure is reducing complexity during trading sessions. Every additional variable your brain has to process compresses the time available for each decision. Under time pressure, the brain defaults to the fastest shortcut available. And the fastest shortcut when a trade is in profit is: close it before something bad happens. Trading fewer instruments, using fewer indicators, and limiting the number of open positions simultaneously gives the brain more space to evaluate each situation on its merits rather than reacting from a default pessimistic position.

Finally, and most importantly: track it. You cannot manage a bias you cannot see. Automated behavioural analytics remove the subjectivity from the evaluation. TradeMedic simulates what would have happened if the trader had not manually closed their profitable trades. The trader can see, across hundreds of trades, whether their manual closes improved their performance or hurt it. For most traders, the answer is clear: the manual closes are costing them money. Seeing that in black and white, backed by their own data, is more powerful than any amount of advice about letting profits run.

What does the data show about taking profits too early?

Across a dataset of 500,000+ trader accounts, TradeMedic detects and quantifies several patterns directly connected to pessimism bias. The cut-profits-early analysis simulates the outcome of every trade that was manually closed in profit, calculating what the result would have been if the trade had been left to run to its take-profit or stop-loss level. For traders where the simulation shows they would have been better off not closing manually, the system quantifies the exact cost of their early exits.

The stop accuracy analysis provides the other side of the picture. With 5.9% of traders showing too-wide stops in their top 5 issues (versus 0.2% showing too-tight stops), the data confirms that traders overwhelmingly err on the protective side when placing stops. These are not separate problems. They are two expressions of the same underlying psychology: a systematic overestimation of the probability that something will go wrong.

The overoptimism analysis adds a third dimension: 8% of traders set take-profit levels that are too ambitious (10% among profitable traders, 7% among loss-making traders). Combined with early manual closes, this means a significant number of traders set targets they never intend to let the market reach. They plan for 80 pips, close at 15, and the data shows they would have been better off with a target of 40 that they actually let play out.

What makes this data valuable is that it turns an invisible bias into a visible pattern. A trader who suspects they cut profits early but is not sure can see the evidence in their own trading history. And a trader who thinks their stop placement is fine can see whether the data agrees. The pessimism bias does not announce itself. But its effects are measurable across every dimension of trade management.

Small wins and large losses are not bad luck

Most traders who struggle with profitability describe their problem as bad luck, bad timing, or a strategy that is not quite right. Very few identify the real pattern: they are systematically making their wins smaller and their losses larger because of how their brain processes the probability of things going wrong. The pessimism bias is invisible in any single trade. You close a trade in profit. That feels like the right decision. It is only across hundreds of trades that the pattern becomes visible and the cost becomes undeniable.

The traders who perform well over time are not the ones who are more optimistic. They are the ones who have systems in place that prevent their pessimism from dictating trade management decisions. Whether that means partial closes, breakeven stops, or automated analytics that show them what their early exits are actually costing, the common thread is that they have separated the decision to manage risk from the emotional impulse to avoid any possibility of a negative outcome. The bias is not going away. The question is whether you build around it or let it run your trading.