Reward Risk Imbalance: When Winning is Not Enough

Success in trading is often judged by how frequently a trader wins. A high hit rate can feel validating as a sign of mastery, discipline, and insight. Yet, behind this comforting illusion often lies a quiet distortion that erodes performance over time: Reward–Risk Imbalance.

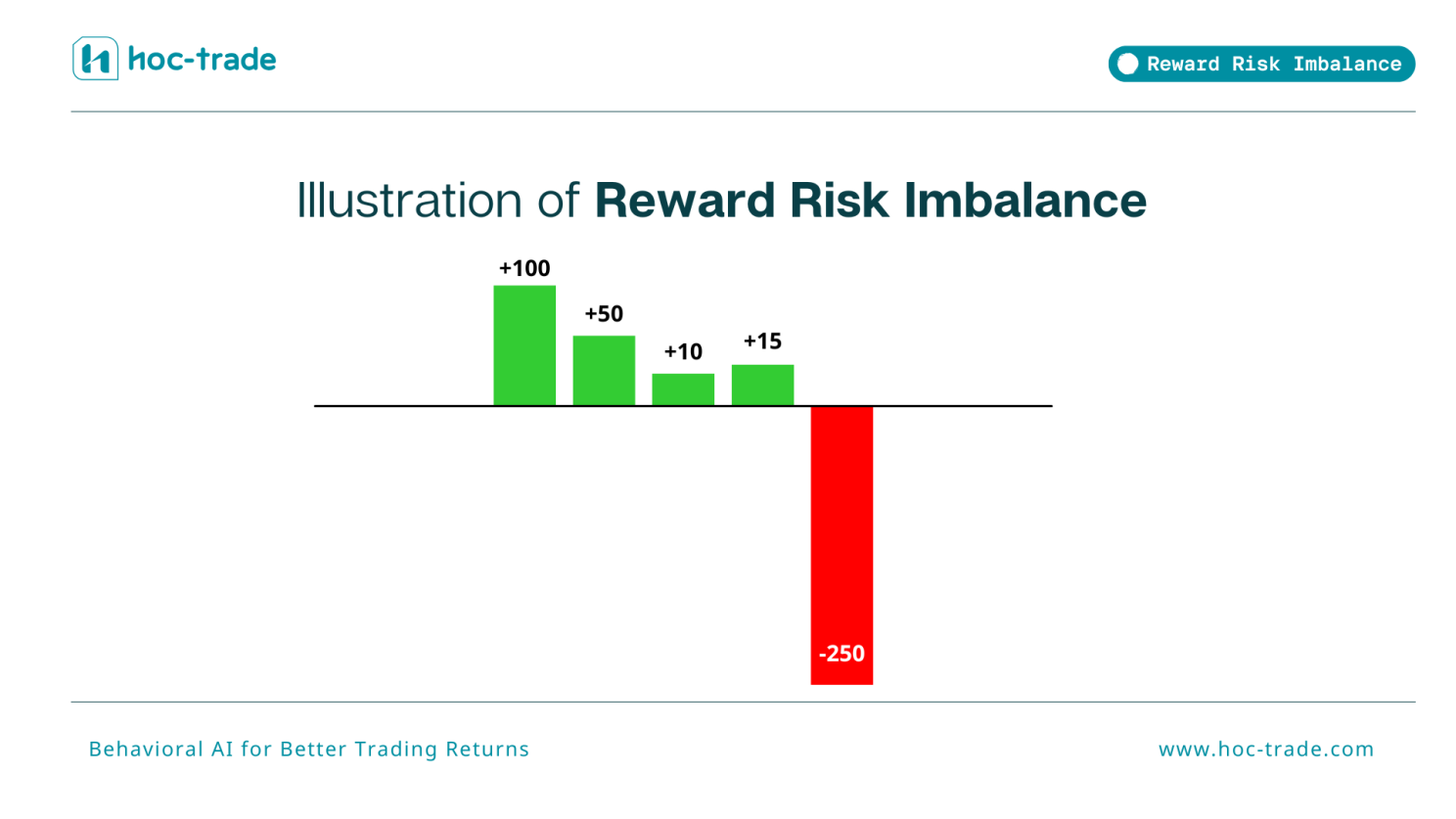

This imbalance occurs when traders lose more in losing trade than they gain in winning ones. On the surface, it sounds like a simple math problem, but its implications reach much deeper. Even a trader who wins 60% of the time may struggle to stay profitable if the average loss per trade outweighs the average profit. The outcome is a fragile system where consistency masks inefficiency where one large loss can undo the cumulative effort of many smaller wins.

What is the risk-to-reward ratio in trading?

At the foundation of this imbalance is the Reward–Risk Ratio (RRR), a measure of how much potential profit a trader expects relative to the amount they risk losing. A well-structured RRR allows traders to remain profitable even with a modest win rate. In theory, this ratio is embedded in every trading plan through the placement of take-profit and stop-loss levels.

In practice, however, the designed RRR often diverges from the executed RRR. Trades that start with a clear risk boundary may end up being manually closed, adjusted, or extended beyond their original parameters. What begins as strategic flexibility can easily evolve into emotional improvisation, where the logic of a system gives way to the impulses of the moment.

Why do traders with high win rates still lose money?

Reward–Risk Imbalance rarely emerges from reckless intent. It grows from subtle emotional patterns that distort decision-making. Fear often drives traders to secure profits too early, while hope keeps them holding onto losses longer than planned. Small adjustments such as widened stop or shortened take-profit feel rational in the moment but gradually erode the intended edge.

These reactions stem from loss aversion, which makes the pain of losing twice as strong as the pleasure of winning, and overconfidence, which encourages traders to underestimate downside exposure after a few successful trades. The result is a self-reinforcing cycle where frequent small wins build false confidence, while occasional large losses undo progress and trigger further emotional decision-making.

Over time, this pattern transforms trading from a statistical exercise into a psychological loop, where control feels present, but imbalance quietly dictates the outcome.

Not all Reward–Risk Ratios are inherently good or bad. A low ratio, where the potential gain is smaller than the potential loss, can still be effective if the hit rate, or probability of success, remains high enough. Likewise, a high ratio such as five or ten to one can be profitable even with a lower win rate. Each trading strategy carries its own relationship between the Reward–Risk Ratio and the hit rate, and profitability depends on how well these variables align over time. Find a dedicated analysis on how well RRR and win rate predict profitability here.

Designing systems and RRR targets based on data provides a strong foundation, but it is only the beginning. What traders plan in theory often diverges from what they execute in practice. The realized Reward–Risk Ratio frequently tells a different story, one shaped not by design but by emotion and behavior.

How does TradeMedic detect reward-risk imbalance?

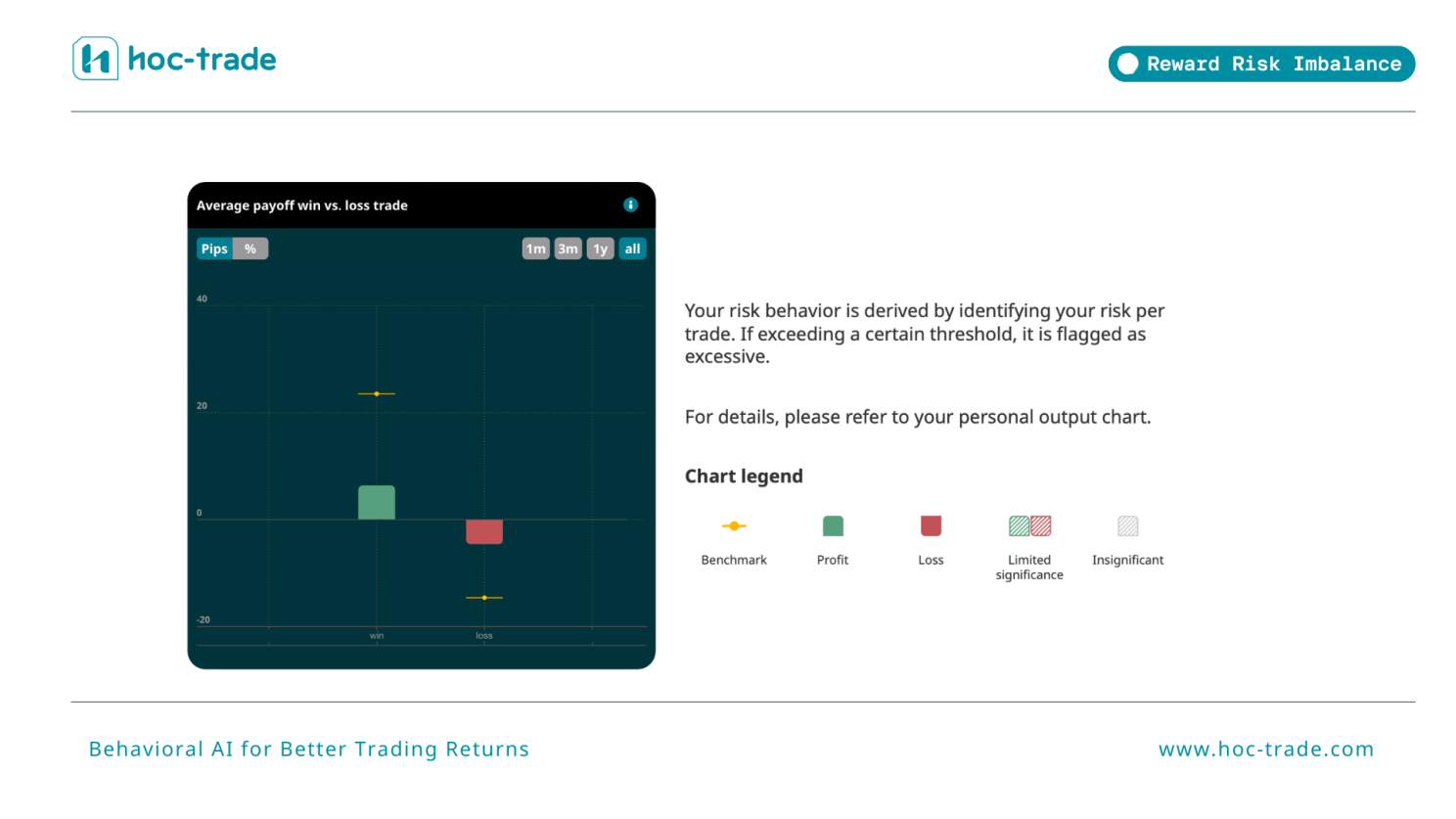

Hoc-trade’s Behavioral AI translates this concept into measurable insight by analyzing the actual outcomes of executed trades. Rather than relying on the trader’s intended plan, the system examines the realized behavior behind each position. It compares the average profit and average loss across all trades, expressed in both pips and returns, to detect whether a trader’s losses consistently outweigh their gains.

When the average loss exceeds the average profit, Hoc-trade identifies a Reward–Risk Imbalance. While this does not mean that necessarily something is wrong with the strategy (it could be a successful scalping strategy with small gains and high hit rate), we have found that it oftentimes is a very good indicator that the actually realized RRR differs significantly from the RRR within the trading strategy. To do so, Hoc-trade classifies trades as either profit or loss, then calculates the averages to uncover behavioral tendencies that erode long-term performance.

Through this data-driven reflection, traders can see how often they deviate from their own intentions and how those small deviations accumulate into measurable imbalance. By visualizing where confidence turns into exposure and where small deviations compound into loss, it helps traders rebuild consistency with data-driven insights.

Reward Risk Imbalance in Trading Explained

How to fix a poor risk-to-reward ratio

Recognizing imbalance is the first step toward improvement, but change happens only when traders begin to measure proportion instead of frequency. True progress comes from aligning intent with execution; following through predefined exit rules, reviewing average profit and loss over time, and confronting the emotional impulses that distort discipline.

Reward–Risk Imbalance ultimately reminds us of that success in trading is not about being right more often but about ensuring that every loss costs less than what a win earns. Profitability stems from proportion, not prediction. And the strongest traders are those who let mathematics, not emotion, define their edge.

TradeMedic AI analyses over 60 behavioral patterns, including Reward Risk Imbalance across 500,000+ trader accounts. Visit TradeMedic to see how it works and get your own personal analysis.

Watch Why Reward-Risk Imbalance Matters When Winning is Not Enough