Confirmation Bias in Trading: Why Traders Ignore What the Market Is Telling Them

Confirmation bias is the tendency to seek, interpret, and remember information in a way that confirms what you already believe. The term was coined by psychologist Peter Wason in 1960 after an experiment that revealed something uncomfortable about human reasoning: when given a simple number sequence and asked to discover the underlying rule, more than half of his participants failed. Not because the rule was complex. Because they only tested examples that matched their initial guess. They never tried to prove themselves wrong.

In trading, this plays out constantly. You form a view on a market. You look at charts, read analysis, check the news. And without realising it, you give more weight to anything that supports your position and less weight to anything that contradicts it. The result is a feeling of being well-informed and thoroughly prepared, right up until the trade goes against you and you can't understand why.

What makes confirmation bias particularly dangerous in financial markets is the nature of the data itself. Markets produce continuous, ambiguous information that can almost always be read in multiple ways. The same price action that looks like a pullback to one trader looks like a trend reversal to another. This ambiguity is where confirmation bias thrives. In a laboratory, a wrong hypothesis gets disproven quickly. In a trading account, a biased thesis can survive for days or weeks because the trader keeps finding new reasons to believe it, until the account balance forces the truth.

What is confirmation bias?

Confirmation bias is a cognitive bias first demonstrated by Peter Wason at University College London. In his 1960 experiment, participants were given the number sequence 2-4-6 and told it satisfied a rule. Their task was to figure out the rule by proposing their own sequences. Most participants assumed the rule was "even numbers going up by two" and tested sequences like 8-10-12 or 20-22-24. These all satisfied the actual rule, which was simply "any three ascending numbers." But because participants never tested sequences that would disprove their hypothesis, like 1-2-3 or 5-11-40, they never discovered it.

Raymond Nickerson's comprehensive 1998 review in the Review of General Psychology described confirmation bias as "the seeking or interpreting of evidence in ways that are partial to existing beliefs, expectations, or a hypothesis in hand." His review identified the bias across medicine, law, science, and everyday reasoning, though notably did not cover financial markets. Research applying confirmation bias to trading and investing has only gained traction in the last two decades.

Two psychological mechanisms drive it. The first is challenge avoidance: people prefer not to discover they are wrong. The second is reinforcement seeking: people actively want to find out they are right. In trading, both mechanisms run simultaneously. A trader with an open position has a financial incentive layered on top of the cognitive bias. Being wrong doesn't just feel uncomfortable. It costs money. So the motivation to filter information becomes even stronger than in Wason's lab.

How does confirmation bias show up in trading?

Confirmation bias rarely announces itself. It doesn't feel like a mistake while it's happening. It feels like thorough research. That's what makes it different from more obvious errors like revenge trading or overtrading, where most traders can at least recognise the behaviour after the fact. With confirmation bias, the analysis process itself is compromised, and the trader never sees it.

Here are the most common ways it appears in real trading behaviour.

Fighting the trend. A trader forms a directional view based on their analysis, then selectively processes information that supports it while the market moves against them. They notice bullish signals on the chart and skip over bearish ones. They read macro commentary that agrees with their position and dismiss contrary views as uninformed. The conviction that "I am right, the market is wrong" persists until the stop loss gets hit or the account forces a reassessment. TradeMedic's data across 500,000+ trader accounts detects this as the Fighting the Trend pattern, where traders show consistent losses on positions entered against the prevailing short-term and medium-term trend direction.

Moving stop losses further away. When a trade moves into loss territory, the trader doesn't re-evaluate the thesis. Instead, they look for a new reason to stay in. They find a support level on a lower timeframe, or a Fibonacci retracement that happens to sit near the current price. These levels may be technically weak, but they serve a psychological purpose: they confirm the belief that the trade will recover. TradeMedic detects this as the Fail to Cut Losses pattern, where traders who widen their stop losses during a trade would have performed better if they had kept the original stop in place.

Doubling down into losing positions. The same mechanism as moving stops, but more aggressive. Each dip gets reframed as "a better entry" rather than evidence the thesis was wrong. The trader searches for reasons the price will reverse. In TradeMedic's dataset, roughly 20% of all traders show doubling down as a significant pattern, but only 5% of profitable traders do. That gap tells a clear story: the traders who are making money are the ones willing to accept when a trade isn't working.

Hedging instead of closing. Rather than admitting the original trade was wrong and taking the loss, a trader adds a hedge. This preserves the belief that the initial position will eventually work out while adding complexity and transaction costs. The hedge is a cognitive compromise: it lets the trader avoid confronting disconfirming evidence while appearing to manage risk. TradeMedic identifies this as Inefficient Hedging, where hedged positions underperform non-hedged positions for that trader.

Setting unrealistic profit targets. Overoptimism in take profit levels is partly driven by confirmation bias. The trader selectively focuses on best-case scenarios for how far price could run, underweighting the base rate of typical price movements in that instrument. They remember the one time price hit an ambitious target and forget the five times it reversed before getting there. Research on optimism bias shows that people systematically overestimate the likelihood of positive events happening to them, creating a feeling of control over outcomes they cannot actually influence. In trading, this translates directly into take profit levels that look reasonable on paper but rarely get hit in practice.

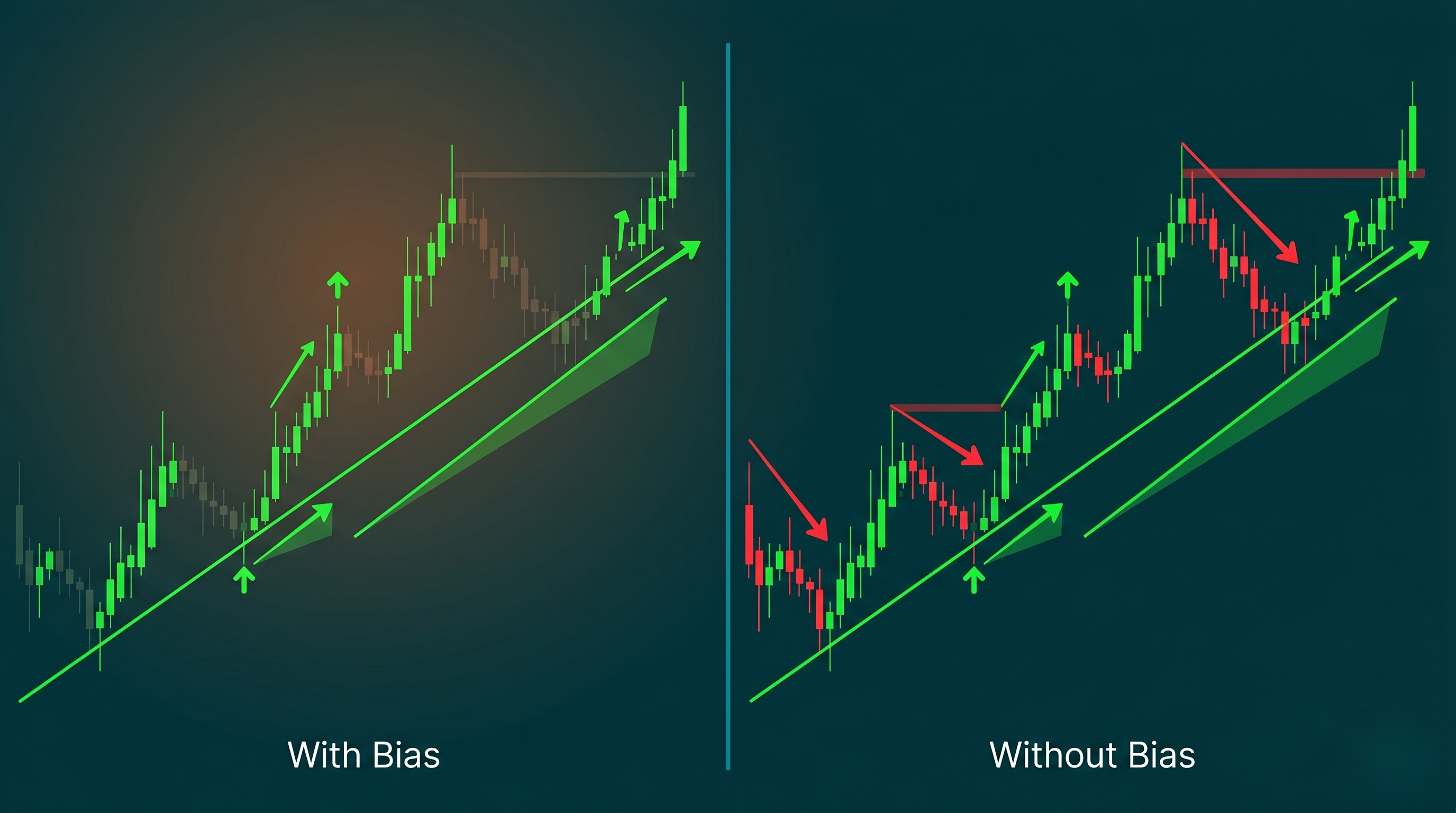

Selective chart reading. This is one of the most common and least discussed manifestations. A trader who is bullish scans the chart for bullish patterns: double bottoms, ascending triangles, hidden bullish divergence. They skip bearish signals on the same chart. When the current timeframe looks unfavourable, they switch to a higher timeframe that still supports their view. When their usual indicators disagree with the trade, they add a new indicator that agrees. They aren't analysing the market. They're assembling a case for a decision they've already made.

Shifting the evidence threshold after entry. Before entering a trade, a disciplined trader might require three independent signals to align. But once the position is open, the threshold drops. A single bullish candle becomes "the market is turning." A minor bounce off a support level becomes "the thesis is confirmed." The commitment to the position changes how much evidence the trader needs to feel validated, and how much they need to feel concerned.

What are the most common examples of confirmation bias in trading?

The trend fighter. A trader goes long on EUR/USD based on their fundamental analysis. Price breaks below a key support level. Instead of closing the position or re-evaluating, they switch from the one-hour chart to the weekly chart, which still looks constructive. They find a Fibonacci level near the current price. They read a macro piece mentioning potential USD weakness. None of these data points individually would have convinced them to enter a fresh long at this price. But strung together, they justify staying in a losing trade. The trader didn't analyse the market after entry. They defended a position.

The echo chamber trader. A trader opens a long position on gold after reading a bullish thread on X. Over the next two days, the algorithm serves them more bullish gold content because that's what they engaged with. They see three more analysts calling for higher prices, a macro thread about central bank buying, and a chart showing a cup-and-handle formation. Price drops. They hold, because "everyone I follow is still bullish." What they don't see is the bearish analysis the algorithm deprioritised: the rising real yields, the DXY breakout, the COT positioning showing crowded longs. They didn't choose to ignore those signals. The platform chose for them, and confirmation bias made sure they didn't notice.

The stop loss mover. A trader is short GBP/USD with a stop at 1.2750. Price moves against them to 1.2730. They notice a resistance level at 1.2780 on a lower timeframe and move the stop to 1.2785. Price pulls back briefly, and the trader feels validated. Then price pushes through 1.2780. They find another level at 1.2820 and move the stop again. Each adjustment feels rational because they found a "technical reason." But the pattern is clear in hindsight: they weren't analysing support and resistance. They were searching for levels that would let them stay in the trade. This is the Fail to Cut Losses pattern, and confirmation bias is the mechanism that made each stop adjustment feel justified.

Why is confirmation bias harder to detect than other trading mistakes?

Most trading errors feel wrong in the moment or at least in hindsight. Revenge trading feels impulsive. Overtrading feels manic. Missing a stop loss feels reckless. Confirmation bias is different. It feels like rigour. The trader has checked the charts, read the analysis, consulted their indicators, and reviewed multiple sources. The research was thorough. The problem is that the entire research process was filtered through a predetermined conclusion.

This connects directly to another bias we've covered on this blog: blind spot bias. Blind spot bias is the belief that "other traders have biases, but I make rational decisions based on evidence." It's the reason confirmation bias survives unchallenged. If you believe your information processing is objective, you have no reason to question it. This is also why simply telling traders to "be aware of confirmation bias" rarely changes behaviour. The bias is, by definition, invisible to the person experiencing it.

Social media has added a new layer to this problem. A 2024 analysis published by the CFA Institute examined how platform algorithms amplify confirmation bias among investors. X (formerly Twitter) curates feeds based on interaction history, meaning a trader with a bullish outlook progressively receives more bullish content. Reddit's upvote and downvote system suppresses minority views, so dissenting analysis on a popular stock gets buried while confirming analysis gets amplified. YouTube recommends videos similar to ones you've already watched. The result is an information environment that narrows over time to match the trader's existing beliefs, without the trader noticing it's happening.

For the retail forex and CFD trader, this is especially relevant. Many traders source a significant portion of their market analysis from social media, Discord groups, and Telegram channels. These environments naturally reward consensus and penalise dissent. A trader in a bullish gold group who posts a bearish chart gets ignored or challenged. A trader who posts a bullish chart gets engagement and validation. The group doesn't make the trader wrong. But it does make them more certain than the evidence warrants.

How does confirmation bias connect to other trading biases?

Confirmation bias rarely acts alone. It interacts with other cognitive biases in ways that compound its effect on trading decisions. Understanding these connections matters because fixing one bias without addressing the others often just shifts the problem.

Loss aversion and confirmation bias. These two form a destructive loop. Loss aversion, the well-documented finding that losses hurt roughly 2.5 to 3 times as much as equivalent gains feel good, makes a trader emotionally unwilling to accept a loss. Confirmation bias then provides the intellectual justification for staying in the trade: "I found a new support level," "the fundamentals haven't changed," "this analyst agrees with me." Loss aversion is the emotional force. Confirmation bias is the rationalisation mechanism. Together they explain the Fail to Cut Losses pattern and much of the behaviour behind widening stop losses.

Overconfidence and confirmation bias. A 2013 field experiment by Park, Konana, Gu, Kumar, and Raghunathan studied 502 investors on South Korea's largest stock message board. They found that investors who showed stronger confirmation bias also showed greater overconfidence, traded more frequently, expected higher returns, and achieved lower realised returns. The mechanism is straightforward: when you only see evidence that you're right, you become increasingly certain of your own judgment. That certainty then makes you dismiss contradictory evidence even more aggressively, creating a self-reinforcing cycle.

Sunk cost fallacy and confirmation bias. Once a trader has invested time in research, built a detailed analysis, and committed capital to a position, the sunk cost fallacy makes them reluctant to walk away. Confirmation bias then supplies the reasons to stay: selective chart reading, favourable analyst quotes, bullish news interpreted as supportive. This combination is particularly visible in the doubling down pattern. In TradeMedic's dataset, roughly 20% of traders show doubling down as a significant pattern. Among profitable traders, that number drops to just 5%. Profitable traders are not immune to sunk costs. They are simply more willing to override the impulse and accept the loss.

Anchoring bias and confirmation bias. The entry price becomes a psychological anchor. When a trade moves against the trader, they don't evaluate the position based on current market conditions. They evaluate it relative to their entry price. Confirmation bias then selectively surfaces information suggesting the price will return to that level. The two biases work together: anchoring distorts the reference point, and confirmation bias distorts the information processing around it.

Gambler's fallacy and confirmation bias. After a string of losses, the gambler's fallacy generates the belief that a win is "due." Confirmation bias then finds the setup that "proves" the turnaround is here. The trader enters with lower-quality analysis than usual because the emotional need for a win has lowered the evidence threshold. If the trade also loses, the cycle restarts. In TradeMedic's data, revenge trading affects 40% of all traders and is the second most common improvement opportunity in the entire dataset. Confirmation bias is one of the cognitive mechanisms that makes revenge trading possible: it's the filter that convinces the trader the next entry is a good one.

How can traders reduce the impact of confirmation bias?

The uncomfortable truth about confirmation bias is that awareness alone doesn't fix it. Knowing the definition, understanding the research, even reading this article: none of it prevents the bias from operating in real time. The bias functions below the level of conscious reasoning. You don't decide to filter information. You do it automatically. That said, structural countermeasures can reduce its impact significantly.

Pre-commit to invalidation criteria before every trade. Before entering a position, write down what would prove the thesis wrong. Not what would confirm it. If EUR/USD breaks below 1.0750, the trade is invalid. If the support level at 1.0800 doesn't hold by the London close, the position gets closed. A stop loss is the most fundamental invalidation tool a trader has. Setting one before entry and committing not to move it removes the single biggest opportunity for confirmation bias to intervene. Traders who trade without a stop loss are especially vulnerable because every price movement becomes an open question that the biased mind can answer however it wants. These criteria need to be specific, measurable, and locked in before the trade is placed. Once you're in the position, the cognitive incentive to move the goalposts is too strong to resist with willpower alone.

Actively seek the opposing case. For every bullish reason you've found, find one bearish reason from a source you don't normally follow. This is uncomfortable by design. The discomfort is the signal it's working. If you find yourself dismissing the bearish case quickly, that's worth paying attention to. It may be genuinely weak, or you may be doing exactly what Wason's subjects did: testing only the hypothesis you already hold.

Lock your analytical tools before the session. Define your timeframe, indicators, and chart setup before you start looking for trades. No switching to the weekly chart to find a bullish signal when the daily is bearish. No adding a Fibonacci retracement after you've already decided to enter. If the analysis framework is fixed, confirmation bias has less room to operate. It can still influence how you read the signals, but at least it can't change which signals you look at.

Journal losses with the same depth as wins. Record what went wrong mechanically, not narratively. "Stop was hit at 1.0740, price continued to 1.0680, thesis was wrong on trend direction" tells you more than "got stopped out, market was choppy." If you find that your loss entries are consistently shorter and less detailed than your win entries, that's confirmation bias showing up in your self-reflection process. A trading journal that only reinforces what you're doing right isn't helping you improve.

Curate your information sources deliberately. If your social media feed, Discord group, or Telegram channel only shows you one side of the market, your information diet is biased regardless of how much of it you consume. Follow at least two analysts who regularly disagree with your default market view. Unfollow accounts that only post confirming analysis. The CFA Institute research shows that algorithm-curated feeds progressively narrow your information environment. Manual, deliberate curation is the countermeasure.

Let data detect what self-reflection can't. This is the structural argument for automated behavioural analytics. Confirmation bias is, by definition, invisible to the person experiencing it. You cannot reliably self-report a bias whose primary feature is making you feel well-informed and objective. TradeMedic AI analyses trading data across 60+ behavioural patterns, including the downstream effects of confirmation bias: Fighting the Trend, Fail to Cut Losses, Inefficient Hedging, Doubling Down, and Overoptimism. These patterns show up in the data whether or not the trader recognises the bias driving them.

What does the data show about confirmation bias in trading?

Confirmation bias doesn't appear as a single line item in a trading report. It's a cause, not a symptom. You can't measure it directly from trade data the way you can measure revenge trading or overtrading. What you can measure are the behavioural patterns it produces, and those patterns are surprisingly common.

Across TradeMedic's dataset of 500,000+ trader accounts, the patterns most directly linked to confirmation bias include some of the most prevalent improvement opportunities detected. Overtrading appears in 31% of all traders, and loss-making traders are more than twice as likely to show it. Doubling down appears in roughly 20% of all traders, but only 5% of profitable traders. Revenge trading, where confirmation bias helps rationalise re-entering after a loss, affects 40% of all traders and is the second most common pattern in the entire dataset.

The gap between profitable and unprofitable traders on these patterns is telling. It's not that profitable traders are immune to confirmation bias. They almost certainly aren't. But the data suggests they've built systems or habits that limit its downstream effects. They fight the trend less. They double down less. They cut losses earlier. Whether that comes from better self-awareness, stricter rules, or automated safeguards varies by trader. What the data shows consistently is the behavioural difference between those who let confirmation bias run unchecked and those who constrain it.

Not a single trader with more than 1,000 trades in the dataset had zero improvement areas. Every trader, including the profitable ones, shows patterns that confirmation bias could be contributing to. The question isn't whether you have the bias. It's how much it's costing you.

The bottom line

The real danger of confirmation bias isn't that it makes you wrong. It's that it makes you feel right while you're wrong. It doesn't feel like a mistake. It feels like being thorough. And that's precisely why it survives in traders who are smart, experienced, and genuinely trying to improve.

The patterns confirmation bias produces, from fighting the trend to doubling down into losing positions, are measurable in trading data. You may not be able to see the bias operating in real time. But the footprint it leaves in your trade history is visible to the right tools.

TradeMedic AI analyses over 60 behavioural patterns, including those driven by confirmation bias, across 500,000+ trader accounts. Visit TradeMedic to see how it works.